USD and yields reverse at their highs, stocks rebound

* Dollar and Treasury yields give up fresh gains ahead of Wednesday’s US CPI

* Stocks closed mixed as traders await bank earnings and data

* Oil extends rally on tighter global supplies amid Russia sanctions

* Bitcoin touches lowest level since November below $95,000

FX: USD has risen 15 out of 16 straight weeks. More cycle highs were made above 110 as bonds sold off some more, pushing Treasury yields north. The 10-year hit 4.80%, seemingly on its way to 5% and huge psychological resistance. But sellers emerged around the US stock market close with the Dollar Index printing a bearish shooting start candlestick.

EUR fell below the key cycle low at 1.0222 from earlier in the month, and the 1.02 figure before paring losses modestly. There is a long-term Fib retracement level (61.8%) of 2022-2023 comeback at 1.0202. Prices bounced back above this late in the session. Elevated tariff and trade risks continue, while already stagnant growth and limited fiscal consolidation means the burden is on the ECB to cut rates and do the heavy lifting. We could hear less dovish commentary from some ECB officials to help support the euro.

GBP sunk to new lows at 1.2099 around lunchtime in the European session before paring some losses. Sterling is obviously not benefitting from higher Gilt yields due to fiscal and inflation worries. There is a slew of UK data this week including CPI on Wednesday. There aren’t many positives for the pound at the moment, though yields didn’t make fresh highs yesterday. Strong inflation numbers push yields higher, soft data raises rate cut bets, so both could hurt the pitiful pound. The bullish candlestick offers technical players some help that the selling could possibly ease up.

USD/JPY turned lower after making new highs at 158.87 on Friday. That is in the intervention zone around 158/160 and may have caused the major to turn down yesterday. In fact, the yen outperformed, with bets on a rate hike at the BoJ meeting next Friday now increased to around a coin toss.

AUD moved to another cycle low at 0.6130 and through the long-term bottom at 0.6169. That was its lowest level since the pandemic in 2020. But prices rebounded as the aussie also outperformed. Tariff angst, fears over economic growth in China and repricing in domestic interest rate expectations have all weighed. USD/CAD is stuck in a range between 1.43 and 1.4450. Solid Canada jobs just about held back all the US dollar buying but tariffs and the uncertain political domestic situation is weighing.

US stocks: Major US stock indices made a dramatic turnaround after opening up over 1% lower. The S&P 500 finished 0.16% higher at 5836. The tech-heavy Nasdaq closed 0.30% lower at 20,784. The Dow settled 0.86% higher at 42,297. Big US financial institutions like Goldman Sachs and Citigroup are set to report earnings later this week. Moderna slumped nearly 17% after the drugmaker cut its full-year revenue outlook. Expect sizeable moves like these in the next few weeks on companies with high expectations and valuations that miss estimates.

Asian stocks: Futures are mixed. Indices kicked off the week mostly lower on the hot NFP report and jump in bond yields. The Nikkei 225 was closed for a holiday. The ASX 200 again saw tech and also financials drag on the index amid strength in energy. China was subdued and didn’t benefit from better-than-expected trade data, even after determined comments from officials about supporting the economy.

Gold succumbed to the higher dollar and yields after four days of buying. Risk off sentiment and haven buying had seen gold move to record highs in several currencies, including AUD, CAD, EUR, and GBP.

Day Ahead – King Dollar rules

The greenback has gained close to 10% since the lows in September. Of course, Trump 2.0 is meant to help the dollar with a mix of deregulation, tax cuts and other measures to boost the world’s biggest economy. The December FOMC meeting also helped too as it kicked off a more hawkish stance by the Fed. Rate cuts have been unwound with barely over one quarter point rate cut for the whole of 2025 now priced in. That doesn’t happen until September with some questioning if the next move will be a hike.

US exceptionalism is the enduring theme with last week’s bumper jobs data continuing the narrative and further boosting yields and the dollar. Does the US actually need pro-growth Trump policies when the economy seems very solid at present? Or is his bark bigger than his bite (buy the rumour, sell the fact) once the inauguration is over on 20 January?

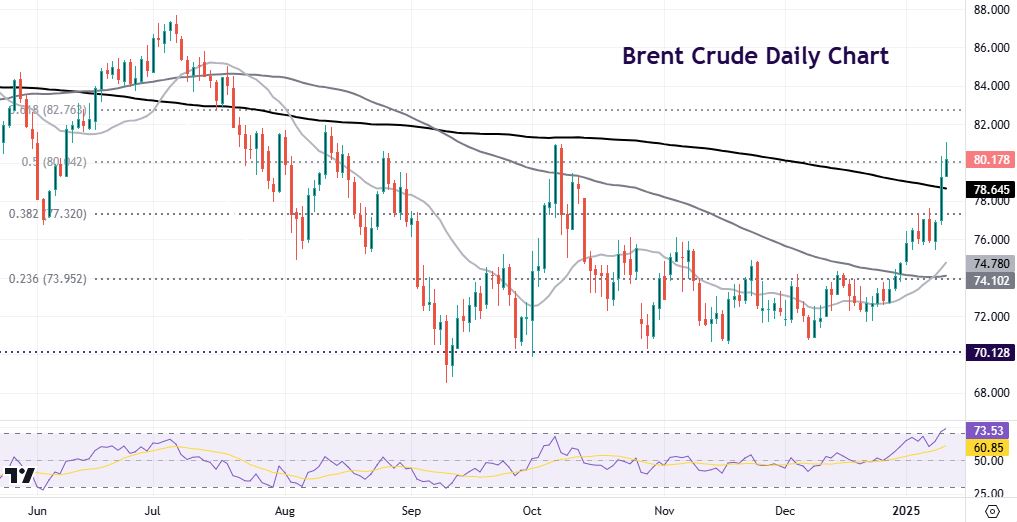

Chart of the Day – Oil on a tear…

Markets are increasingly worried about inflation, as bond yields surge higher across the world. To add to these price pressures, crude prices has rallied strongly this year up over 7%. Recent stricter US sanctions on Russian oil have targeted both production and export flows. These latest sanctions have the potential to erase the surplus many oil analysts forecast for the oil market in 2025. However, as we saw following the EU ban on Russian oil and products imports, Russia managed to redirect trade flows, which meant little impact on their export volumes. What President Trump does too will have an impact.

Brent crude has broken to the upside over the last two sessions after bullish consolidation around $76. Prices also pushed up above the 200-day SMA at $78.64. The midpoint of the April to September fall sits at $80.04. the Fib level above here (61.8%) is at $82.76. Prices are overbought so a correction may be imminent. The 38.2% Fib level below is $77.32.